The world looked different coming out of COVID in 2021. Face masks, hand sanitizer and vaccine cards were physical proof that things had changed. As some of us headed back to work, we noticed that many co-workers would not make that same decision. Offices once filled with the energy of a full staff were now empty rooms peppered with deserted desks and the whispers of the remaining survivors. Zoom calls replaced the conference room table and fist bumps replaced the handshake. Had the business world changed forever?

Early 2022 brought another change that was less noticeable than the empty offices. A series of small interest rate increases started to compound casting downward pressure on the real estate market and exacerbating the existing COVID-caused vacancies. The black swan event had now given birth to an ugly duckling.

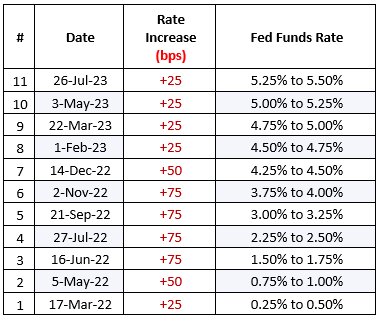

The cost of borrowing money has an impact on nearly every financial decision that a business, consumer and investor will make. After hitting record lows in 2020 and 2021, interest rates climbed to a 23-year high in 2023. Federal fund rates were around zero as recently as the first quarter of 2022. Since then, there have been 11 rate increases, totaling +500 basis points in 18 months. And, there is rampant speculation that there will be another increase before the end of the year.

The table below shows when the Federal Open Market Committee (FOMC) changed interest rates, the amount of each rate change in basis point (“bps”) and the resulting federal funds rate range (the suggested target rate range where commercial banks borrow and lend).

The Federal Funds Rate is one of the most important components of the U.S. economy. Its impact spans the entire economy including commerce, investments, employment growth and inflation. The stock market typically reacts very strongly to changes in this fund rate. It can influence interest rates for everything from home and auto loans to credit cards. Investors keep a close watch on it and small fluctuations can translate into big swings in an investment calculation.

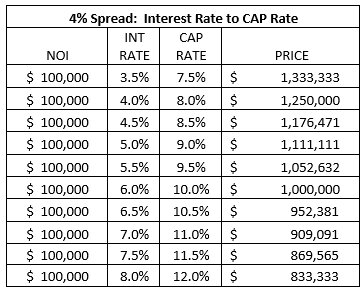

From a real estate perspective, these increases have significant consequences on the overall sale price of a property and the net rate of return an investor must achieve. Investors will often borrow money to purchase a property and target a specific margin between the cost of borrowing that money and the target return on the investment. Said differently, there must be a spread between the interest rate and CAP rate. CAP rate, or capitalization rate, is a real estate valuation measure used to compare the ratio of return on an investment. The CAP rate is determined by dividing the net operating income (NOI) by the sale price. The model below assumes that an investor is looking for a 4% spread between the cost of money and the cost of the property. As interest rates increase, and that same 4% spread is maintained, it significantly decreases the price an investor can pay for the same $100,000 of income (NOI).

Staying informed about the current trends and factors affecting the commercial real estate market is crucial for making informed investment decisions. This is especially true when the conditions are rapidly changing. I, myself, as a commercial property owner, investor and broker, look to fact patterns such as these to help provide the necessary insights, risk assessments and predictive models, to my partners and clients which gives them a competitive edge in the dynamic and ever-changing commercial real estate industry.

Please feel free to reach out in confidence for a confidential, no-obligation conversation about your real estate. Brian Rossi, brossi@bellcornerstone.com.

*BellCornerstone is the Nation’s Leader in Newspaper Real Estate.